Structured settlements are designed to protect injury victims from financial whiplash.

Instead of a one-time lump sum, they provide guaranteed payments over time, offering long-term stability when income or health is uncertain.

That predictability is why structured settlements are being used more than ever, surging 58% in just two years—from $6 billion in 2022 to $9.48 billion in 2024.

But as reliable as structured settlements are, personal circumstances change. Emergencies arise, goals shift, and future payments don’t always solve today’s problems.

That’s where selling some or all of a structured settlement payment stream comes into play.

If you’re considering this option, this guide explains how to sell structured settlement payments step by step and how to decide whether selling makes financial sense for you.

Key takeaways

- Selling is easy. Deciding to sell isn’t

The mechanics of selling structured settlement payments are straightforward, but the real risk lies in the decisions you make before and after the sale. A bad call on timing, amount, or terms can cost you future income. - Only sell if the tradeoff clearly solves a real problem

Selling makes sense when you have a specific, time-sensitive need for cash. It usually doesn’t make sense if there is no urgent use for the money. - Legal and pricing details matter more than speed

Not all settlements can be sold, and not all buyers offer fair deals. Reviewing your contract, understanding state law, and getting multiple quotes protects you from unnecessary discounts and hidden costs. - Court approval exists to protect you, not slow you down

Judges review sales to ensure you understand the deal and that it is fair under your circumstances. This step is required in every state and is especially strict for minors. - If selling isn’t the right move, earn money in the background with Settlemate

Instead of giving up future income, Settlemate helps you improve your financial position gradually by finding and claiming money you’re already legally owed from class action settlements, refunds, and recalls. It works passively, requires almost no effort, and complements longer-term financial decisions without adding debt or risk.

How to sell structured settlement payments: 10 key steps

While selling structured settlement payments is procedurally straightforward, the choices you make before the sale and the implications after the money reaches your account often matter more than the transaction itself.

Below are 10 key steps to selling structured settlement payments the right way.

Step 1: Decide if selling is a good idea

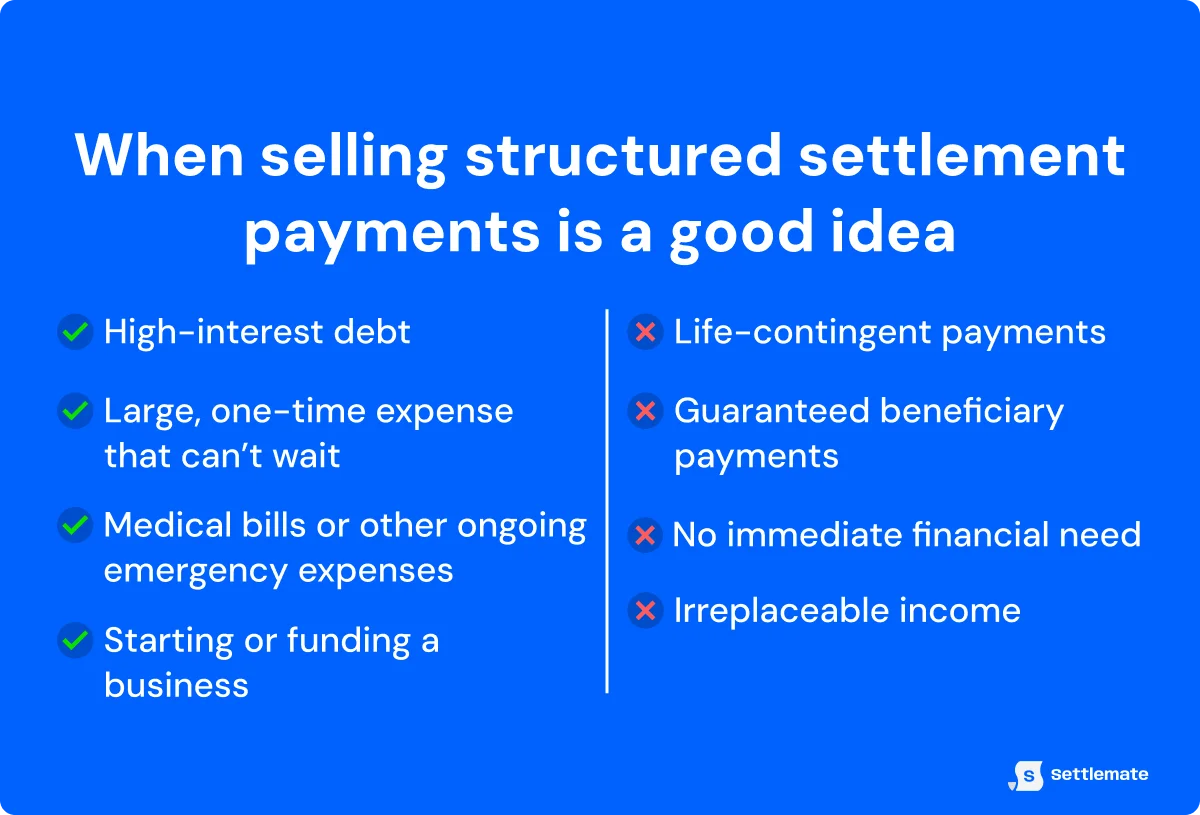

People usually choose to sell structured settlement payments for one simple reason: they need access to cash now. Common reasons include:

- Paying medical bills or other emergency expenses

- Covering tuition or education costs

- Paying down high-interest debt

- Starting or funding a business

- Covering a large, one-time expense that can’t wait

As urgent as these situations may be, selling future payments is still a tradeoff. You’re giving up a guaranteed income in exchange for a smaller lump sum today. If that lump sum doesn’t clearly solve the problem in front of you, selling doesn’t make sense.

Selling may not be a smart move in these situations as well:

- Life-contingent payments: If your payments stop when you die, buyers take on more risk and offer steep discounts, which usually results in poor value.

- Guaranteed beneficiary payments: If your payments are guaranteed to a beneficiary, selling them transfers those rights to the buyer instead.

- No immediate financial need: If you don’t have a specific, time-sensitive use for the money, selling often creates more long-term cost than benefit.

- Irreplaceable income: If selling eliminates income you can’t realistically replace later, it can weaken your financial stability.

Step 2: Confirm you’re allowed to sell your payments

Simply deciding you want to sell structured settlement payments isn’t enough. You also have to be legally allowed to sell them—something that depends on your settlement terms and state law.

To check whether a sale is allowed, review your structured settlement agreement, annuity contract, and any court orders tied to your case. Look for restrictions such as:

- Non-assignment language: Your settlement may include language that restricts or prohibits transferring your payment rights to another party, which can limit or prevent a sale.

- Minimum sale amounts: Some settlements require you to sell a minimum number of payments or dollar amount, making small or partial sales impossible.

- Restrictions tied to child support, disability benefits, or bankruptcy: Existing legal obligations or court orders may restrict your ability to sell payments or require additional approvals before a transfer is allowed.

You can also consult a lawyer to help you with this part. Although you’re not required to hire one, this is often a smart move since the buyer’s lawyer who files the court case represents the buyer’s interests, not yours.

Step 3: Decide what to sell

At this point, the question becomes how much you should sell.

You have two options:

- Sell all remaining payments and receive no future income.

- Sell only a portion, such as specific payments or a set dollar amount, and keep the rest.

In many cases, selling fewer payments preserves long-term stability while still solving the immediate problem.

Step 4: Research buyers and get multiple quotes

Structured settlement payments are purchased by factoring companies—businesses that specialize in exchanging future payments for cash today. Not all buyers price deals the same, so who you work with matters.

Start by researching potential buyers, then request quotes from at least three companies.

Using multiple quotes gives you leverage, exposes hidden fees, and helps you avoid over-discounting your payments. Make sure every quote is based on the same set of payments.

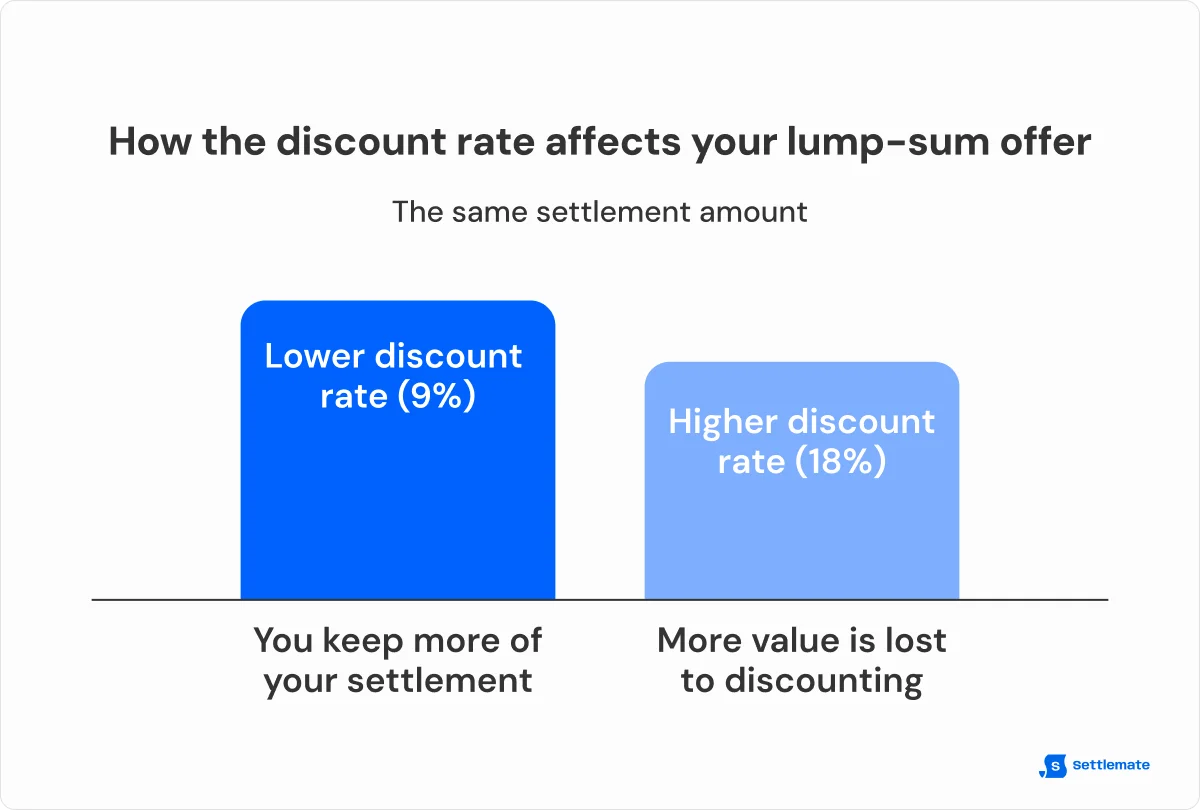

As far as quotes go, factoring companies calculate offers using a present-value formula.

Because you’re getting paid early, the lump sum will always be less than the total value of the payments.

The key variable is the discount rate, which typically ranges from 9% to 18%. Lower is better here since you keep more of your money.

Other factors that might affect your offer include:

- Interest rates

- Number and timing of payments

- Current market rates

- Economic conditions, including inflation

- Service and processing fees

Step 5: Submit an application and complete underwriting

Once you choose an offer, the buyer will have you complete an application and submit supporting documents. This allows them to verify:

- Your identity

- Your payment schedule

- The details of your settlement

During underwriting, the buyer confirms your payment stream with the annuity issuer and checks that there are no competing assignments or legal conflicts.

If anything is missing or unclear, expect follow-up requests before the deal can move forward.

Step 6: Review the contract carefully and insist on clear numbers

Before you sign anything, read the contract line by line. Your priorities should be to:

- Verify the payments being sold: Confirm that the payment dates, amounts, and number of payments match what you agreed to.

- Confirm your net payout: Ensure the exact amount you’ll receive and how it will be delivered are clearly stated.

- Review key contract terms: Look for clauses covering cancellations, penalties, arbitration, confidentiality, and who pays legal or court costs.

Step 7: Get court approval and attend the hearing

All US states have Structured Settlement Protection Acts designed to prevent unfair or predatory transfers. One of their core requirements is that any sale of structured settlement payments receive court approval.

While the factoring company typically prepares and files the court petition, you’ll need to review it, sign supporting declarations, and cooperate throughout the process.

After the filing, the court schedules a hearing where a judge reviews the deal and asks you questions directly to confirm the sale is in your best interest.

Judges typically focus on:

- Your financial situation and purpose for selling

- Your understanding of the discount rate and fees

- The presence of dependents who rely on the payments

- The consideration of alternatives to selling

- The fairness and reasonableness of the deal under state law

At the hearing, bring valid ID and be prepared to clearly explain what you’re selling, why you’re selling it, and how you plan to use the money. If the judge has concerns, they may limit the sale, require changes, or deny approval.

You should also know that selling a structured settlement that belongs to a minor is significantly more restricted.

Courts require clear proof that there is an immediate need for cash and that selling is genuinely in the child’s best interest. These rules exist to protect funds intended for a minor’s future, and they’re strictly enforced. That’s why some buyers won’t purchase minor-related payments at all.

Step 8: Receive the court order and finalize the transfer

Once the court approves the sale, a signed order is issued and sent to the annuity issuer or structured settlement obligor—the party legally responsible for making your settlement payments. The issuer then updates its records to redirect the sold payments to the buyer.

From filing to approval, the court process typically takes 45 to 60 days, depending on state law, court availability, and whether all documents were submitted correctly.

Step 9: Get funded and confirm delivery details

After the transfer is finalized, you receive your lump sum by check or wire, as outlined in the contract.

Before considering the process complete, you should confirm the amount matches the agreed-upon net payout.

Step 10: Understand what comes after the sale

While the sale itself may be officially complete, your responsibilities might not be. There are three post-sale considerations to keep in mind:

- Payment issues: If there’s any issue with payment redirection, notify the buyer and the annuity issuer immediately.

- Repeat sales risk: Be cautious about selling again too quickly since repeat sales stack discount costs.

- Cash discipline: If the lump sum is meant for a specific purpose, follow through promptly to avoid the money getting absorbed into everyday spending.

Then, there’s also the issue of taxes.

In most cases, selling structured settlement payments is tax-free, just like receiving the payments over time, especially when the settlement is tied to physical injury or disability, and the transfer is court-approved.

However, taxable situations still exist.

Settlements tied to lost wages unrelated to physical injury, emotional distress, or punitive damages may have tax implications. A large lump sum can also affect your overall tax picture, placing you in a higher tax bracket.

That’s why it’s crucial to confirm how the sale affects your taxes and consult a tax or financial professional if needed, especially before filing your next return.

To sell or not to sell: The pros and cons of selling structured settlement payments

In certain situations, selling structured settlement payments can be a practical financial move, as it gives you:

- Access to cash: A lump sum can cover major, time-sensitive expenses without taking on new debt.

- Debt relief: Selling can provide enough liquidity to pay off high-interest debt all at once, reducing long-term financial strain.

- More control today: Some people prefer managing a larger sum now rather than waiting for smaller payments over time.

- Reduced financial stress: Eliminating urgent financial pressure can provide real peace of mind.

However, selling structured settlement payments also comes with real tradeoffs, including:

- You receive less overall: Buyers apply a discount rate, meaning you give up a portion of the total value of your future payments.

- You lose long-term income: Selling reduces or eliminates a guaranteed payment stream designed to provide stability over time.

- The process takes time: Court approval is required, so funding isn’t immediate.

- Mistakes are expensive: Selling too much or selling repeatedly can compound losses and weaken long-term financial security.

It’s important to emphasize that selling structured settlement payments isn’t inherently right or wrong. The only question is whether the tradeoffs make sense for your situation, timeline, and future income needs.

If they don’t, there are other paths that you can consider:

Earn money in the background with Settlemate

While you’re making larger financial moves and deciding whether to sell structured settlement payments, you can also look for ways to bring in incremental cash without making almost any active effort.

All you need is Settlemate.

This app helps you find and claim money you’re already legally owed from class action settlements, product recalls, price-drop refunds, and similar refund opportunities—money that often goes unclaimed simply because people don’t know it exists or don’t want to deal with the paperwork.

Settlemate steps in and does the following:

- Finds money you’re legally owed: It matches you to open class action settlements and refunds based on your purchases and profile.

- Automates the work: The app scans emails and receipts, auto-fills claim forms, and submits them for you.

- Removes friction: You don’t need any lawyers, paperwork, or manual searches.

- Keeps you informed: Settlemate tracks claim status, deadlines, and payout estimates in one place.

- Works passively: The app alerts you when new opportunities open, so you don’t have to look for them.

Download Settlemate on the App Store or Google Play to improve your financial position over time while you work through longer-term decisions.