.png)

After allegations of cheating on emissions tests and deceiving customers, Volkswagen paid a whopping $14.7 billion settlement in 2016. Many car owners who joined the class action lawsuit received $5,000 to $10,000 compensation, and that’s only about 0.000068% of the total settlement amount.

Where did the rest of the money go?

Before payments reach class members, portions of the settlement must cover lawsuit costs, incentive awards for lead plaintiffs who started the class action, and administrative costs. Plus, class actions count thousands or even millions of members, and payout amounts also depend on the number of valid claims filed.

This guide explains how settlement money is divided, who gets paid first, why payouts vary, and what determines the amount individual claimants receive. You’ll also find out how Settlemate can help you claim your portion of the settlement within minutes.

What is settlement distribution in a class action?

A class action settlement is when a company agrees to resolve claims brought on behalf of a large group of people affected by the same issue out of court, instead of going to trial. This usually happens in the case of:

- Data breaches, such as a medical data breach

- Defective products

- False advertising

- Employment violations

- Privacy lawsuits

Instead of each person filing an individual lawsuit, eligible individuals become part of a settlement class that shares a single settlement fund.

Settlement fund distribution refers to the process of dividing and paying out the settlement fund after the case resolves. The funds typically aren’t distributed to class members directly or simultaneously.

Before payouts are issued, the settlement fund may be used to cover any existing legal fees. The remaining funds are then distributed among eligible class members in accordance with the terms of the settlement agreement. In some cases, every class member receives the same amount. In others, payouts depend on factors such as documented loss, the severity of the claimant's injury, or the level of participation in the proceedings.

Because many class actions involve thousands or millions of people, settlement distribution can take months to complete.

How are settlements distributed in a class action lawsuit?

Although every class action is governed by a distinct settlement agreement, most distributions follow the same general process, which involves:

- Creating the settlement fund

- Deducting legal and administrative costs

- Determining who qualifies for a payout

- Defining lead plaintiff service awards

- Calculating and distributing individual payouts

1. Creating the settlement fund

Once both sides agree to settle, the court reviews the proposed agreement to make sure it’s fair, reasonable, and adequate for the entire class. This is called final approval.

After approval, the defendant deposits the agreed settlement amount into a dedicated settlement fund. This fund is used to cover all expenses incurred during the settlement process.

In some cases, the defendant funds the settlement in a single lump-sum payment, while in others, payments may be made in installments. This is especially the case in large-scale settlements.

The settlement fund is typically managed by a third-party administrator or held in a supervised escrow or trust account until distribution begins.

2. Deducting legal and administrative costs

Before class members receive payments, the court-approved costs of running the lawsuit and settlement process are deducted from the settlement fund. These costs include lawyer fees and administration costs.

Class action attorneys usually work on a contingency fee basis, meaning they only get paid if the case is successful. Because these lawsuits can take years to litigate and often involve extensive discovery, expert witnesses, and multiple appeals, law firms usually absorb the costs and financial risk throughout the case.

Courts review fee requests to ensure they’re reasonable and proportionate to the value of the settlement. They generally use two methods to evaluate attorney fees:

- Percentage of the fund: Attorney fees in class actions commonly range from 20% to 30% of the total settlement amount, though courts sometimes approve higher percentages in unusually risky or complex litigation.

- Lodestar method: Fees are based on hours worked multiplied by reasonable hourly rates.

The following deductions cover the operational side of the settlement process. Below, you can see the typical tasks major claims administrators help manage:

3. Determining who qualifies for a payout

After deductions are approved, the next step is identifying eligible class members and validating claims.

Eligibility depends on the terms outlined in the settlement agreement and varies depending on the type of lawsuit. To qualify, claimants may need to provide documentation to confirm they were part of the affected group during a specific period. Depending on the case, this may include:

- Proof of purchase

- Account ownership or subscription history

- Product or service usage

- Travel records

- Employment history

- Residency in a certain state or region during a specific time period

- Confirmation of being affected by a data breach or incident

Some settlements require extensive documentation, while others allow class members to submit claims with minimal or no proof, especially when the defendant already has custom records. Before payments are approved, the claims validation process involves reviewing the documentation submitted by the claimants, as well as:

- Checking for duplicate submissions

- Screening for fraudulent claims

To reach potential claimants, administrators use multiple communication methods, including:

- Email notices

- Mailed notices

- App notifications

- Public announcements

- Digital ads

- Dedicated settlement websites

Class members are also typically allowed to opt out of the settlement before a specified deadline. It means forfeiting your right to a payout from the class action while preserving the right to pursue an individual lawsuit.

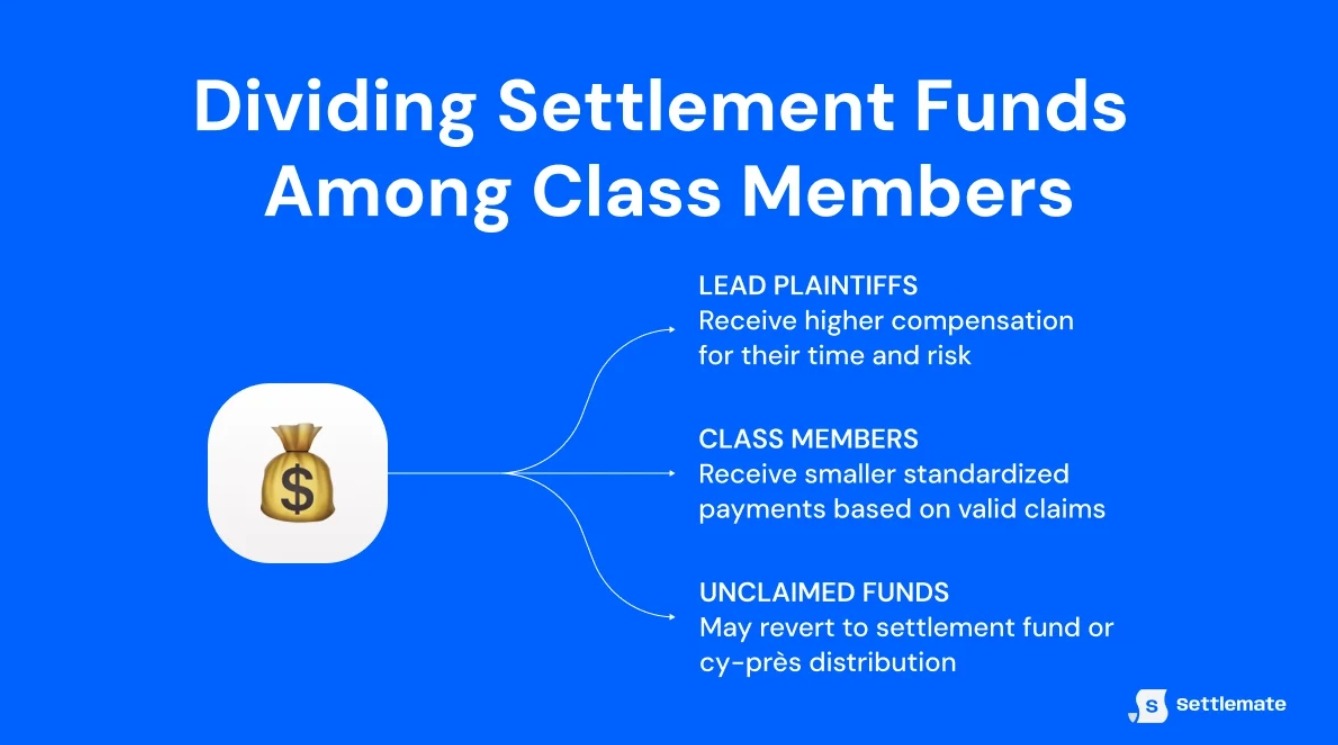

4. Defining lead plaintiff service awards

In many class actions, the named plaintiffs who initiate the lawsuits and represent other claimants receive additional compensation called service awards or incentive awards. These individuals often spend years actively participating in the litigation process by:

- Communicating with attorneys

- Providing documents and records

- Responding to discovery requests

- Attending depositions

- Publicly attaching their names to the lawsuit

Service awards are intended to compensate lead plaintiffs for the extra time, effort, and risk involved in representing the class. These payments are usually modest compared to the overall settlement fund, ranging from a few thousand dollars to tens of thousands of dollars in larger cases. Like attorney fees, service awards must be approved by the court.

Not every class action includes service awards, and they can sometimes be controversial if critics believe lead plaintiffs receive disproportionately large payments.

5. Calculating and distributing individual payouts

Once deductions and awards are finalized, the remaining settlement funds are distributed among eligible class members. The exact payout structure depends on the settlement agreement.

Some class actions divide funds evenly, while others calculate payments based on individual losses or participation levels.

Here’s an overview of the most common settlement distribution models:

Note: In many class action settlements, fewer approved claims result in larger individual payments, while higher participation rates reduce the average payout per claimant.

What happens to unclaimed settlement funds?

Not every eligible individual submits a claim. This is especially the case in large consumer or data breach cases where notices are overlooked, or the payout seems too small to justify the effort. When this happens, the remaining settlement money is redistributed or handled according to the settlement agreement and court approval.

Some settlements include a residual or second distribution phase, in which case the leftover funds are redistributed to eligible class members who already filed valid claims.

If there are still remaining funds after all valid claims are paid, some settlements use a cy pres distribution. This means the remaining funds are donated to nonprofit organizations or groups that are considered related to the subject of the lawsuit and can indirectly benefit the class. These include:

- Consumer protection organizations

- Privacy advocacy groups

- Legal aid organizations

Some settlements include a reversion clause. If not all funds are claimed, the unused money may:

- Return to the defendant

- Reduce the defendant’s total cost exposure

Reversion clauses are negotiated as part of the original agreement.

How is a settlement paid out to claimants?

When the settlement distribution begins, administrators send payments using different methods, often depending on claimant preferences:

Important: Class action settlement payouts are often taxable. In general, compensation tied to lost income or punitive damages must be reported on your tax return, while payments for physical injury may be tax-free.

How long do class action settlement payouts take?

Class action settlement payouts can take months or even years to be fully processed. Even after a case is settled, several legal, administrative, and verification steps must be completed before the funds reach class members.

The exact timeline depends on how large the case is, whether there are appeals, and how quickly the claims are submitted and verified, but it typically looks like this:

Why class action settlement payouts may seem modest compared to the personal injury claim amount

The average class action lawsuit payout per person may seem small compared to the total settlement value. To understand why, it helps to compare class action settlements with personal injury settlements. Although both involve compensation after harm, they work in fundamentally different ways.

In a personal injury settlement, one injured person or a small group of harmed individuals receives compensation based on their individual damages. After the gross settlement is agreed, the following deductions are made:

- Lawyer fees, usually about 33% of the total settlement

- Case costs, including court filing fees, expert witness, medical record retrieval, depositions and transcription costs, as well as investigation and discovery expenses

- Outstanding liens, such as medical, insurance, credit card, government, and workers’ compensation liens

- Pre-settlement funding, if a plaintiff took out a loan to cover living or medical expenses while the case is pending

What’s left is the final payout to one individual. In a class action settlement, one large settlement fund is divided among many people who share similar claims, after all court-approved deductions have been made.

Class action payouts can feel insignificant, and the process may seem complicated enough to skip entirely. But that’s exactly where money gets left behind. A few missed claims over time can add up to hundreds of dollars in compensation you were legally entitled to receive.

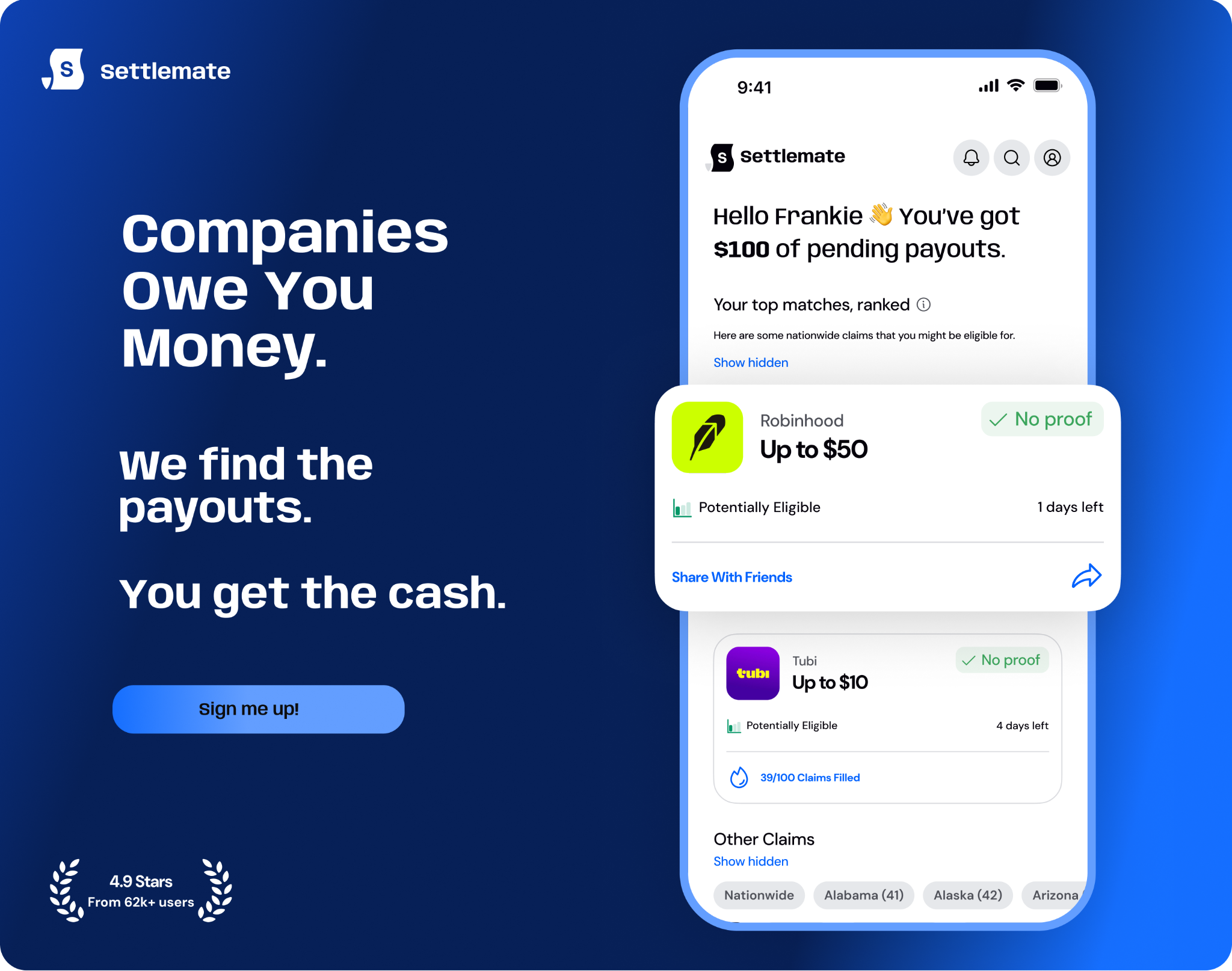

If you want to stop leaving money on the table, sign up for Settlemate — a money claiming app that tracks eligible class action settlements and files the claims for you.

Stay on top of class action payouts with Settlemate

It’s easy to miss a class action settlement notice or a deadline to file a claim. Even when you’re eligible, payouts often go unclaimed because the necessary information gets buried in emails, arrives too late, or feels too time-consuming to act upon.

The Settlemate class action lawsuit app is designed to simplify the claims process. Instead of you having to manually track every settlement notice or figure out whether you qualify, a centralized system helps surface relevant cases, organize documentation, and keep deadlines visible in one place.

Here’s how it works:

- Finding claims you qualify for: Settlemate scans your inbox and receipts to uncover class actions you are eligible for.

- Filing automatically: The app prepares the claim whenever possible, flags missing documentation so you know what to provide, and lets you review and submit the claim in minutes.

- Tracking payouts: You can track your claims’ statuses, estimates, and deadlines in real time.

To get started, download Settlemate from the App Store or Google Play, connect your inbox, and start claiming the money you’re owed.

There’s minimal risk in trying the app. If it doesn’t help you recover at least the cost of the subscription within the first year, you may be eligible for a full refund.