Most people assume that once a company takes their money through hidden fees, false promises, or broken products, that is the end of it. The company wins, and you just have to move on.

That is the myth.

The truth is that U.S. law provides several clear ways to recover what is rightfully yours. Every year, consumers win billions back through class-action settlements, regulator-enforced compensation, and court-ordered payouts. Yet most people never take advantage of these opportunities because they do not know where to begin.

This guide explains exactly how to claim the money from the company with real examples, practical steps, and advice to avoid common mistakes. By the end, you will know how to turn frustration into action and take the money back from the company that owes you.

Key takeaways:

- Know your legal options: You can claim money through class actions, direct refunds, or regulator-ordered settlements when companies break the law.

- Act quickly and file correctly: Submit complete, accurate claim forms before deadlines. Missing details or late submissions are the most common reasons people lose payouts.

- Use your refund rights: Ask for direct refunds on faulty products, unauthorized charges, or canceled services. Laws like the DOT refund rule and state lemon laws protect you.

- Watch for regulator refunds: Agencies such as the CFPB, FTC, and state Attorneys General often send refunds automatically or through simple online claim forms.

- Make it effortless with Settlemate: Settlemate finds eligible claims, fills forms, tracks payouts, and alerts you before deadlines, so you never miss money companies owe you.

What "taking the money from the company" actually means

When we talk about "taking the money," we are not talking about loopholes or tricks. We mean the legitimate, legal pathways through which laws and regulators force companies to return money to consumers after breaking rules, violating contracts, or misleading customers. These are systems built into U.S. law to keep the marketplace fair and to make sure that when companies overstep, they pay up.

Across the U.S., companies quietly distribute billions in refunds and settlements to customers through these programs. Some payments are small, like a $20 refund for a subscription the company charged without your consent. Others are large, like thousands of dollars for a defective car, a misused loan, or a data breach. The challenge is that most people do not know how or where to claim it.

Types of claims – The legal tools to recover your money

There are three main routes for recovering money from a company:

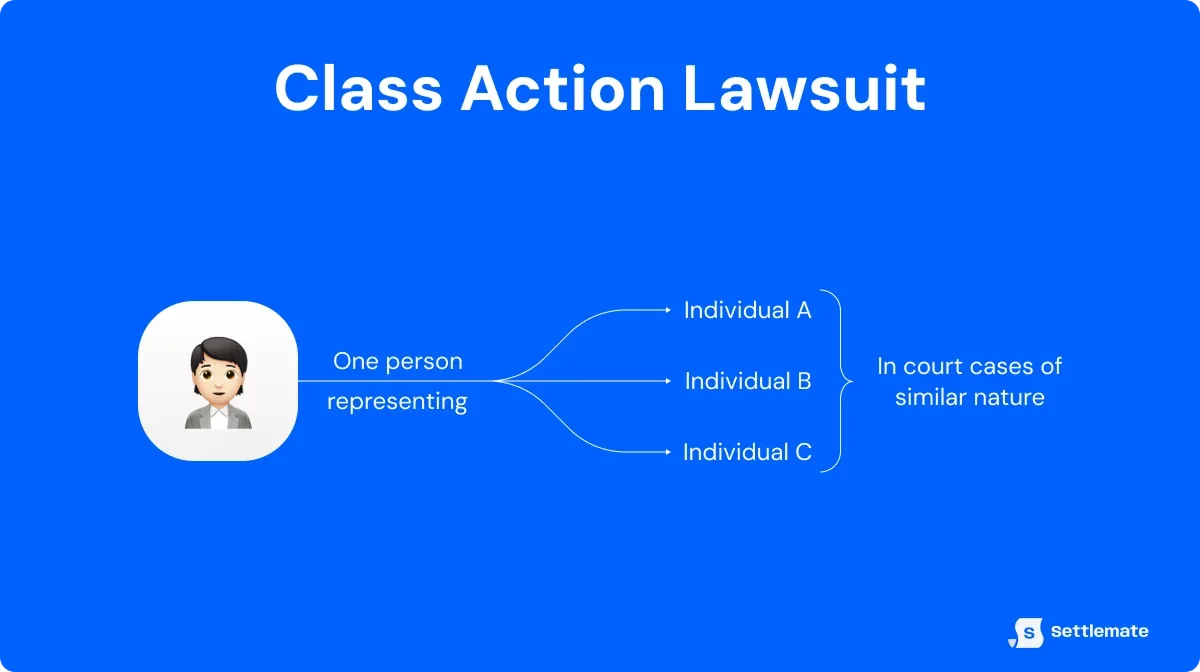

1. Class actions

A class action is a single lawsuit filed on behalf of a large group of consumers who suffered the same harm from one company. Instead of thousands of people each suing over small losses, the court consolidates similar claims into a single case. This collective approach saves time, cuts legal costs, and forces companies to address widespread issues in a single ruling.

For example, the Equifax data breach resulted in a $425 million settlement for approximately 147 million consumers. Class members are people who meet the court's definition, such as those who bought a specific product or appeared in a leaked database.

Why use a class action?

Class actions allow consumers to recover small amounts that would not be practical to pursue individually. Filing a claim usually takes only a few minutes online, and attorney fees come out of the total settlement fund rather than your pocket. Even smaller payments can be worth it when the process is simple and free.

How it works:

Once a class action settles, the court appoints a claims administrator to manage the process from start to finish. Here's what typically happens:

- Notice: Affected consumers receive a notice by mail, email, or public announcement. It explains who qualifies, the claim deadline, and how to file. Always check your inbox and spam folder, since many notices are delivered electronically.

- Claim form: Most settlements that include money require a claim form. This form asks for your contact information and proof of purchase or account activity.

- Gathering information: Prepare documents that demonstrate your qualifications, such as receipts, invoices, or billing statements. If the claim involves an overcharge or defective product, include any record that proves you were affected. Always be truthful, as false claims are illegal and delay legitimate payments.

- Filling out the form: Complete all required sections carefully and sign it. Double-check your address and email, since incorrect details can prevent the administrator from contacting you or sending payment.

- Submitting: Submit the form by mail or online according to the instructions in the notice. Keep a copy or confirmation for your records. Missing the deadline usually means losing your right to payment.

- Tracking: Many settlement websites let you track your claim status. Check periodically for updates, payment approvals, or requests for more information.

Key terms to know:

- Class member: A person who meets the class definition set by the court, such as "all customers of Company X who purchased Y between January 2020 and December 2022."

- Lead plaintiff: The individual or small group representing the entire class.

- Opt-out: The option to exclude yourself from the settlement. If you opt out, you keep the right to sue separately but give up your share of the class payout.

- Settlement administrator: The neutral third party that manages claims and distributes payments.

- Affidavit or verification: A signed statement confirming your claim information is accurate under penalty of perjury.

Real-world class action examples:

- AT&T data breach (2024–2025): AT&T agreed to a $177 million settlement resolving two 2024 breach incidents that exposed customer data. Eligible users can file claims and, with supporting documentation, recover up to several thousand dollars, depending on the losses. The claim deadline is 18 December 2025, the opt-out deadline is 17 November 2025, and the court has set the final approval date for 15 January 2026.

- Visa and Mastercard merchants' chargeback rules (2025): In October 2025, Visa and Mastercard agreed to a $199.5 million settlement with merchants who alleged that the networks coordinated changes to chargeback rules that shifted fraud costs onto businesses without chip-enabled terminals. Visa will pay $119.7 million, and Mastercard will pay $79.8 million, while Discover and American Express settled earlier.

- Clearview AI face-scraping privacy case (2025): In March 2025, a U.S. judge approved a novel nationwide settlement that gives class members a potential 23 percent equity stake in Clearview AI or a share of future revenue under specific triggers, rather than immediate cash. Several states had objected to the structure, but the court found the arrangement fair and reasonable.

2. Refunds, returns, and recalls: direct claims

Getting your money back does not always mean going to court or hiring a lawyer. You can often recover your money through refunds, returns, and recalls if you know how to ask for them and use the rights you already have on your side.

Company refund policies

Most companies will correct an error once you raise the issue. If a product fails, a service is not delivered, or the company charges you the wrong amount, contact customer service and explain the situation clearly.

Have proof of purchase ready, such as a receipt or order number, and request a refund or replacement under the company's warranty or satisfaction guarantee. If the company refuses, mention your rights under consumer laws such as the FTC's Refunds Rule for travel or your state's lemon law.

Lemon laws and warranties

If a product keeps breaking and the manufacturer can't fix it, warranty and lemon law protections apply. These laws require manufacturers to repair, replace, or refund defective items, especially vehicles, appliances, and electronics.

For example, if your new refrigerator or car keeps malfunctioning after several repair attempts, the manufacturer must provide a replacement or issue a refund. You are not required to accept a product that never works properly.

Unauthorized charges

Unauthorized or recurring charges are among the most common refund disputes. If a company continues billing you after cancellation or adds hidden fees, contact your bank or credit card issuer to dispute the charge. Under federal rules, Regulation Z for credit cards and Regulation E for electronic transfers, banks must investigate and correct billing errors. Many banks also issue immediate refunds once you report the problem.

Travel and service refunds

Refund rules for travel have become clearer in recent years. The U.S. Department of Transportation now requires airlines to automatically refund canceled flights within seven days for credit card payments or twenty days for other payment methods.

Cruises, charters, and other federally regulated travel services follow similar requirements. For hotels, events, and similar bookings, review both the company's refund policy and your credit card's purchase protection.

Regulator-forced refunds (without class action)

In some cases, government agencies order companies to return money directly to consumers. A clear example is SmileDirectClub (2023–2024), where the New York Attorney General ordered the company's payment processor to refund $4.8 million to more than 28,000 customers it had continued to charge after closure.

3. Regulatory and agency settlements

Federal and state regulators often force companies to repay consumers directly through enforcement actions and settlement programs. Agencies like the CFPB, FTC, and state Attorneys General regularly turn corporate penalties into real refunds for customers.

CFPB (Consumer Financial Protection Bureau)

The CFPB oversees banks, lenders, debt collectors, and other financial service companies. When it finds violations, the agency can order refunds and use its Civil Penalty Fund to compensate affected consumers.

Notable examples:

- Wells Fargo (2022): The CFPB required the bank to return $2 billion to customers for illegal fees and loan practices, one of the largest restitution orders in U.S. history.

- Tempoe (2024): The CFPB forced the lease-to-own financier to place $191.9 million into a victim fund and send checks to more than 264,000 customers who could not recover the value of their leases.

In most CFPB cases, you do not need to file a claim. The company uses its own records to identify eligible customers and automatically issues payments.

FTC (Federal Trade Commission)

The FTC targets fraud, scams, and unfair business practices across most industries outside of banking. When companies break the rules, the FTC often turns penalties into refund programs managed by a third-party administrator.

For example, in the Gig-work settlement (2025), the FTC recovered $7 million for nearly 100,000 workers after a virtual job platform misled them about pay and opportunities.

If the FTC orders a refund, you may receive a short claim form or a direct payment. The agency emphasizes that it will never charge you a fee or ask for personal information to process your refund. Any call or email demanding payment for your settlement is a scam.

State Attorneys General

Many states have consumer protection laws, and their AGs enforce them. These settlements often produce direct refunds or credits. NY's AG has recovered millions of dollars for consumers from companies that cheat them. Other AGs routinely announce deals, e.g., refunds for utility overcharges, loan servicing errors, and false advertising.

These programs sometimes operate like mini-class actions or regulatory refunds. If your complaint relates to a company's statewide misconduct, check your AG's announcements for consumer recoveries.

The step-by-step playbook: how to claim the money from the company

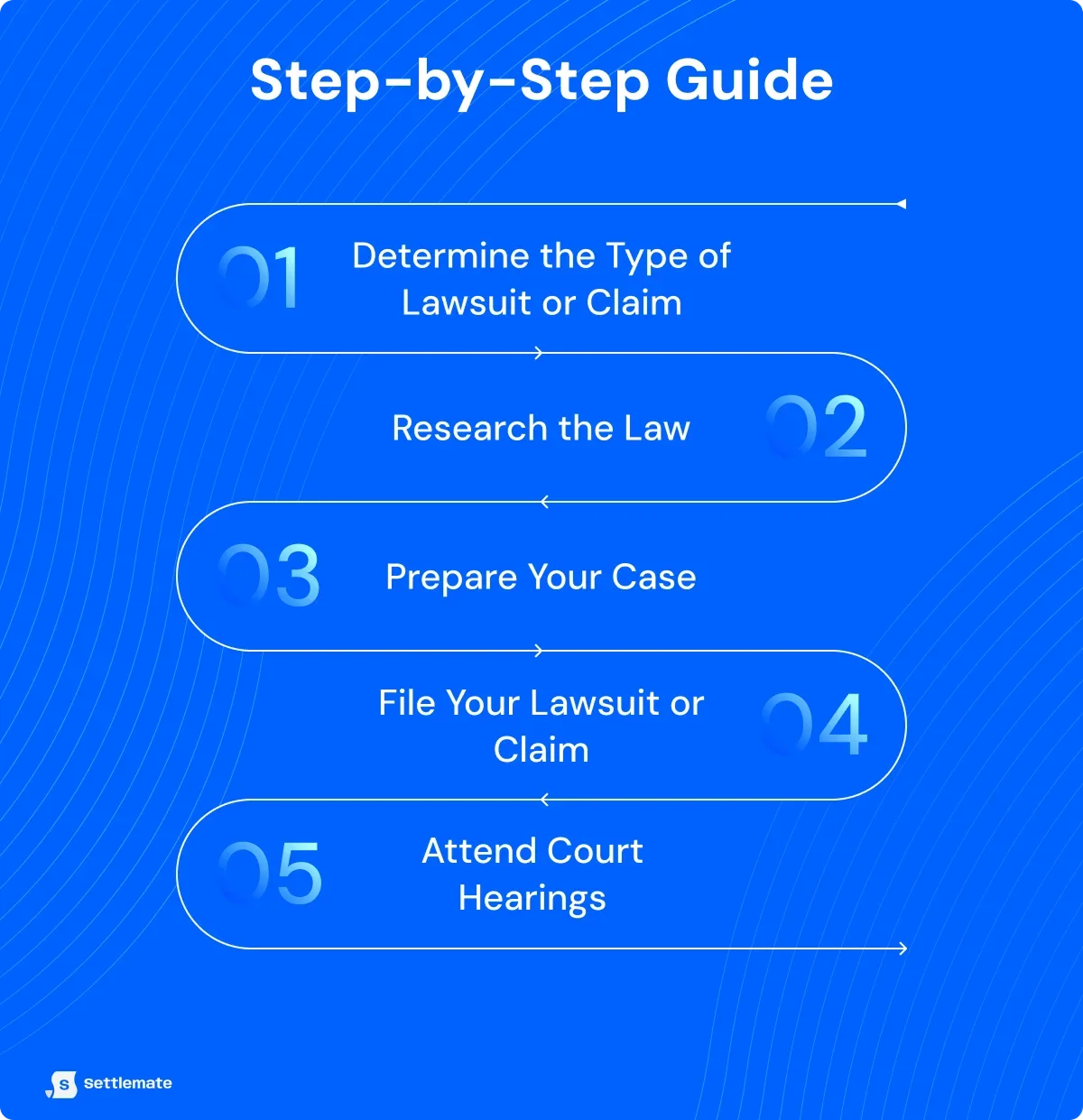

Here's how to move from thinking 'I'm owed money' to actually getting paid:

1. Gather proof

Save every document that shows what happened: receipts, contracts, statements, screenshots, and emails. Solid evidence gives your claim credibility and helps speed up approval.

2. Find where to file

Figure out which channel fits your case:

- If you received a class action notice, follow its official instructions.

- If it's a simple overcharge or defect, contact the company and request a refund.

- If a regulator announced a settlement, check the agency's website for a claim form.

3. Verify the notice

Only act on official notices. Real settlement notices are sent by mail or email, or posted publicly, with clear claim forms, deadlines, and contact details. Avoid anything that asks for payment or personal banking information.

4. Get the claim form

Download or request the official claim form from the settlement website or administrator. If it wasn't sent to you automatically, the notice will list where to get it.

5. Fill it out accurately

Read the instructions carefully and complete all sections. Double-check your name, address, and email, and attach any required proof such as receipts or billing statements. Never exaggerate or include false information, which can undermine your claim.

6. Submit before the deadline

Send or upload your form before the deadline. Administrators almost always reject late submissions. If you mail it, use a trackable service and keep your proof of postage.

7. Track your claim

After submitting, check your claim's status online or through the hotline listed in the notice. If you do not get confirmation within a few weeks, contact the administrator directly to confirm they received your form.

8. Receive payment

Once approved, you'll get your payment by check, PayPal, or direct deposit. Processing can take months, especially for large settlements, so patience is key.

9. Escalate if needed

If you believe you're eligible but still haven't been paid, file a complaint with the CFPB, FTC, or your state Attorney General's office. Agencies can review your case and sometimes trigger enforcement refunds. Even submitting a complaint keeps you on record if future settlements arise.

Avoiding common pitfalls

Here are the mistakes that stop most people from getting paid:

- Missing deadlines: Mark every deadline as soon as you see it. Most class actions allow 60–120 days to file, and regulators set firm cutoffs.

- Incomplete forms: Fill out every field and attach all required documents. Administrators often reject claims that are missing signatures or proof.

- Wrong information: Make sure your name, address, and account details match current records. Even one error can delay or block payment.

- Company pushback: Some companies offer credits or downplay refunds. If a court or regulator ordered repayment, you are legally entitled to cash.

- Scams: Never pay a fee or share bank details for a settlement. The FTC confirms that real administrators never ask for money or personal data.

- Skipping small payouts: Small checks add up, and filing usually takes minutes. Some settlements pay thousands, so always submit your claim.

- Ignoring updates: Check your email and mailbox for requests from the administrator. Missed messages often mean missed payments.

- Taxes: Set aside a portion of any large payout for taxes. Refunds may count as income depending on the settlement.

How to claim the money from the company with Settlemate

We can conclude that the old belief that when companies keep your money and you just move on, no longer holds up. The better reality is that clear rules, active regulators, and easier tools help you claim the money companies owe you without hassle.

That shift turns missed notices and buried refund pages into real payouts.

Here is how Settlemate makes claiming the money from the company repeatable and straightforward:

- Instant eligibility checks: Settlemate scans your purchase history and matches it to active class actions, refunds, and regulatory payouts. You see exactly which claims apply to you today.

- Auto-filled claims: The app prepares forms with verified details, prompts you for any missing documents, and submits them in minutes.

- Real-time tracking: Watch each claim move from submitted to approved to paid. Get alerts when a new matching case appears.

- Deadline reminders: Settlemate reminds you before a claim closes and when a payout is ready. No missed windows and no chasing status emails.

- Built-in alerts: If a company issues a recall or a regulator orders refunds, Settlemate flags it and shows you the next step.

Turn complicated rules into real cash in your account.

Download Settlemate on the App Store or Google Play and start claiming what companies owe you today.