A class action lawsuit can take months or even years to resolve, but bills don’t stop coming while you wait for the settlement. Medical expenses, rent, groceries, and lost income can quickly create financial strain, especially after an injury or employment dispute.

That’s why many plaintiffs consider applying for pre-settlement funding, also called a lawsuit advance. It gives eligible plaintiffs access to money before their case settles.

However, pre-settlement loans can be costly, and the terms aren’t always straightforward.

This guide to pre-settlement funding explains how these arrangements work, who can qualify, how much an advance costs, and how to evaluate if a lawsuit advance makes sense for your situation.

You’ll also learn how Settlemate automates class action settlement claims, helping you recover any compensation you’re owed faster.

What is pre-settlement funding?

Pre-settlement funding is a type of cash advance offered to plaintiffs awaiting a lawsuit settlement or court award. It’s commonly used in personal injury and employment cases where legal proceedings can take a long time to resolve.

The funding company provides money up front in exchange for a portion of the future settlement or verdict. You can borrow up to 20% of the expected settlement. In most cases, repayment only happens if the plaintiff successfully settles or wins the case. Because of this, pre-settlement funding is often described as non-recourse funding.

Pre-settlement funding has many names:

- Lawsuit advance

- Settlement advance

- Lawsuit funding

- Lawsuit loan

- Pre-settlement loan

The terms lawsuit loan or pre-settlement loan can often be misleading because approval is based on the strength of the legal claim rather than credit score, income, or employment history.

Warning: This type of funding may be helpful, but it can get expensive over time. Some agreements include monthly compounding fees that significantly increase the repayment amount if the case takes longer than expected to settle.

Types of pre-settlement financing

There are several types of pre-settlement funding. The biggest difference between them is what happens if the plaintiff loses the case. Understanding these differences is crucial because the funding structure affects financial risk and repayment costs:

Why to consider pre-settlement legal funding

Pre-settlement funding may help you avoid accepting a low settlement too early. Even if your case is strong, it can take a long time to settle, and you may have expenses during the waiting period that increase financial stress and pressure you into settling quickly.

For example, if you’re recovering from an injury caused by someone else’s wrongful actions, you may face significant medical bills and rehabilitation costs, while going for months without a paycheck. In such cases, pre-settlement funding can support you while you wait for the case to resolve.

Additionally, the approval process for pre-settlement funding is usually faster and more accessible than traditional borrowing options. Since repayment is tied to the outcome of the case in non-recourse arrangements, this option also feels less risky than a traditional loan.

People typically use pre-settlement funding to cover urgent expenses, such as:

- Rent or mortgage payments

- Medical bills or rehabilitation costs

- Groceries and utilities

- Credit card bills

- Transportation

- Childcare

How to qualify for a settlement advance loan

Although pre-settlement funding companies focus less on your credit score, existing debt, employment history, or income, that doesn’t mean the approval is guaranteed. They evaluate the strength of your legal claim and if the expected settlement value is enough to cover the advance and associated fees.

Pre-settlement funding companies typically review:

- The type of lawsuit

- The strength of the evidence

- Severity of damages or financial losses

- The likelihood of a successful settlement or verdict

- Estimated payout

- Insurance coverage and available damages

- Defendant's liability and ability to pay a settlement

- The stage of the legal process

In most cases, funding companies also require the plaintiff to have legal representation. Cases handled by an attorney are generally considered less risky because the funding company can communicate directly with counsel. Your lawyer may help with:

- Providing case records and documentation

- Confirming the status of settlement negotiations

- Sharing medical records or evidence

- Reviewing the funding agreement terms

- Coordinating repayment after settlement proceeds are distributed

Pro tip: While you don’t need your lawyer’s permission to obtain pre-settlement funding, it's advisable to consult them so they can explain the potential risks and review the funding terms before you sign the agreement.

What types of lawsuits qualify for pre-settlement loans?

Pre-settlement funding is most commonly associated with personal injury lawsuits. These typically include:

Plaintiffs involved in class actions and mass tort litigations may also be eligible for pre-settlement funding. These cases often involve large groups of people bringing similar claims against the same company or defendant.

Funding companies may consider these cases attractive when there’s strong evidence of widespread harm, large potential settlements, or ongoing multidistrict litigation.

Common examples include:

Important: Workers’ compensation claims may qualify for pre-settlement funding in some states, but eligibility rules vary. Review local laws and discuss your options with an attorney.

How does pre-settlement funding work?

Pre-settlement funding approval may vary slightly among pre-settlement funding companies, but the process typically involves:

- Submitting an application

- Evaluating the case

- Receiving a funding decision and offer

- Receiving the funds

Step 1: Submitting an application

The application process is usually quick and straightforward, as many pre-settlement funding companies have online application forms. You need to submit:

- Basic personal information

- The type of lawsuit

- Details about the injury or damages

- The date of the incident

- Attorney contact information

Many companies advertise same-day approval and don’t charge upfront application fees.

Step 2: Evaluating the case

After receiving the application, the funding company reviews the legal claim to determine whether it qualifies for funding. It evaluates:

- Evidence and liability

- Insurance coverage and defendant assets

- Expected timeline of the case

The company also contacts your attorney to obtain the case record and discuss the status of the lawsuit.

Step 3: Receiving a funding decision and offer

If the funding company believes the case has a strong chance of success, it may approve the application and provide a funding offer. The offer typically outlines:

- Advance amount: How much money you receive upfront

- Fees and rates: How much the funding may cost over time

- Repayment structure: Whether fees compound monthly or use another structure

- Non-recourse terms: Whether payment is only required after a successful outcome

Step 4: Receiving the funds

After signing the agreement, you often receive funds quickly, sometimes within 24–48 hours, depending on the provider and how soon the attorney provides documentation.

While you usually can’t cover legal services with this funding, you can generally use it for any other purpose.

Note: Receiving pre-settlement funding has little or no long-term impact on your credit score.

What’s the cost of class action lawsuit pre-settlement funding?

Pre-settlement funding can provide financial relief, but it’s one of the most expensive forms of consumer financing.

Most providers charge a combination of fees and financing costs that are repaid directly from your future settlement verdict. Common costs may include:

What are pre-settlement funding interest rates?

Pre-settlement funding rates commonly range from 2% to 5% per month. This may not seem extreme initially, but the monthly rates can accumulate to thousands of dollars via compounding fees over time.

One of the most important provisions in any funding agreement is whether charges use simple interest or compound interest:

- Simple interest applies only to the original advance amount, so costs grow more slowly and predictably.

- Compound interest accrues on both the original balance and previously accumulated charges, so repayment can increase rapidly over time.

Some companies also offer tiered or bucket pricing, where repayment jumps at set time intervals. While costs are more predictable in this case, they can still become substantial.

For example:

Warning: Class action and MDL cases often involve longer timelines than individual personal injury claims. Appeals, settlement negotiations, multidistrict proceedings, and payout administration can delay compensation for years. Funding costs continue accumulating while you wait for the payout.

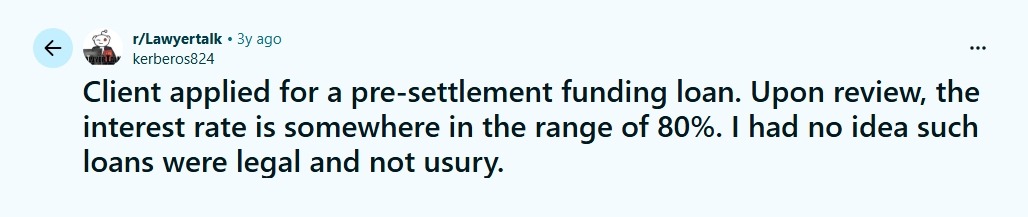

Discussions among attorneys online frequently describe situations where compounding funding charges consumed a large share of the plaintiff’s recovery. Some lawyers warn clients against taking out these advances, describing funding companies as predatory.

Pros and cons of pre-settlement lawsuit funding

Before accepting any funding agreement, weigh both the benefits and potential risks carefully:

How to find the right pre-settlement funding lender

If you decide to get a settlement advance funding, compare multiple providers so you can identify those that offer:

- Lower monthly fees

- Simple instead of compound interest

- Lower administrative fees

- More transparent repayment terms

- Clear communication and customer support

To understand the long-term financial impact of obtaining pre-settlement funding, ask the following questions:

- Are there origination or underwriting fees?

- How much would repayment be after 6, 12, or 24 months?

- Is there a cap on repayment?

- Are additional advances allowed?

- Are there any additional administrative charges?

Because the lawsuit funding isn’t regulated uniformly across states, research any lender carefully before agreeing to funding. Here’s what to pay attention to:

Tip: Borrow only the amount you truly need as every additional dollar can significantly reduce your settlement payout. Treat pre-settlement funding as a short-term emergency option rather than long-term financial support.

What are the alternatives to pre-settlement loans?

Before accepting a lawsuit advance, you may consider exploring alternative financing options, such as:

- Medical payment plans

- Credit union loans

- Financial assistance programs

- Insurance benefits

Additionally, before you borrow against a future settlement, it’s worth checking whether there’s money you may already be entitled to recover.

Billions of dollars tied to class action settlements, product recalls, price adjustments, airline compensation claims, and other overlooked refunds go unclaimed every year. In many cases, people don’t realize they qualify, miss filing deadlines, or don’t have time to handle the claim process.

If you want to find out which compensations you may be entitled to and claim them effortlessly, you will benefit from an app like Settlemate.

How Settlemate helps you recover the money you're owed

Instead of taking on expensive funding immediately, recovering money you’re already entitled to could help reduce short-term financial pressure and limit the amount you need to borrow against a future settlement.

Settlement helps you identify and file claims you may otherwise overlook, including:

- Class action settlements

- Flight delay, flight cancellation, diversion, and other flight disturbance compensation

- Price protection claims

- Refund and overcharge claims

Instead of manually searching for settlements or tracking claim deadlines across multiple websites, you can manage all opportunities in one place and submit claims in minutes. Here’s how it works:

- Eligibility tracking: Settlemate scans your inbox and helps identify active class actions, compensation programs, and refund opportunities you may qualify for.

- Deadline alerts: The app tracks important dates, including claim-filing deadlines and class action opt-out windows, and sends reminders.

- Faster and simpler claim filing: Where available, Settlemate can pre-fill claim forms so you can review, confirm, and submit claims seamlessly.

- Proof guidance: If a claim requires receipts, purchase records, travel confirmations, or other documentation, the app explains what is necessary so you can avoid incomplete submissions and delays.

- Real-time updates: Settlemate notifies you whenever an important milestone is reached, so you’re always up to date on your claim status.

Download Settlemate from the App Store or Google Play, or sign up via the web app today.

Worried about pricing? There’s no downside to trying the app. If it doesn’t pay for itself within the first year, you may be eligible for a full refund under Settlemate’s Value Guarantee.