As many as 60% of Americans will walk away from a purchase the moment pricing gets fishy, making unclear or misleading pricing the top deal-breaker for U.S. shoppers. Surprise fees, vague service charges, “processing” add-ons… nothing kills trust faster.

But what happens when you don’t spot these fees until after you’ve already paid?

That’s when things move from “annoying checkout tricks” to lawsuit territory.

A hidden fees lawsuit has one job: it forces companies to pay back consumers for the money they never should’ve taken in the first place. And because these schemes rarely hit just one person, they almost always turn into class actions.

This article breaks down exactly how these cases work, what past lawsuits have revealed, and where you might be owed cash because a company decided to get “creative” with its pricing.

Key takeaways

- Hidden fees are everywhere and often illegal when not disclosed clearly

Many companies add charges at checkout or on bills. When those fees aren’t clearly explained or advertised up front, they can qualify as deceptive pricing and lead to a hidden fees lawsuit. - You may qualify for open lawsuits without realizing it

Banks, travel sites, telecom providers, and credit card companies have all faced major hidden-fee cases. If the price you paid didn’t match the price you were shown, you may already match one of the active claims. - It’s worth checking your own bills and accounts regularly

Telecom “administrative” fees, travel amenity fees, ticketing “processing” fees, and banking NSF charges are some of the biggest red flags. Spotting these early can help you catch lawsuits you qualify for before the deadline. - New investigations are happening constantly

Lawyers are actively reviewing companies like Uber Eats, SeatGeek, StubHub, and others for drip pricing and junk-fee issues. The list of active cases changes fast, so checking periodically ensures you don't miss potential refunds. - Settlemate helps you claim money you’re legally owed automatically

Instead of digging through bills or hunting for cases yourself, Settlemate scans for eligible settlements, auto-fills your claim forms, tracks payouts, and alerts you to new refunds.

Hidden fees lawsuit: The basics

The average U.S. household burns through $1,495 a year on the hidden costs of simply paying bills. That figure doesn’t even include the surprise add-ons, mystery charges, and service fees that show up everywhere else, from travel bookings to streaming services and everyday purchases.

In other words, you’re paying more than you think, in more places than you realize.

That’s exactly why you need to know what to watch out for and what can turn into a hidden fees lawsuit that puts money back in your pocket.

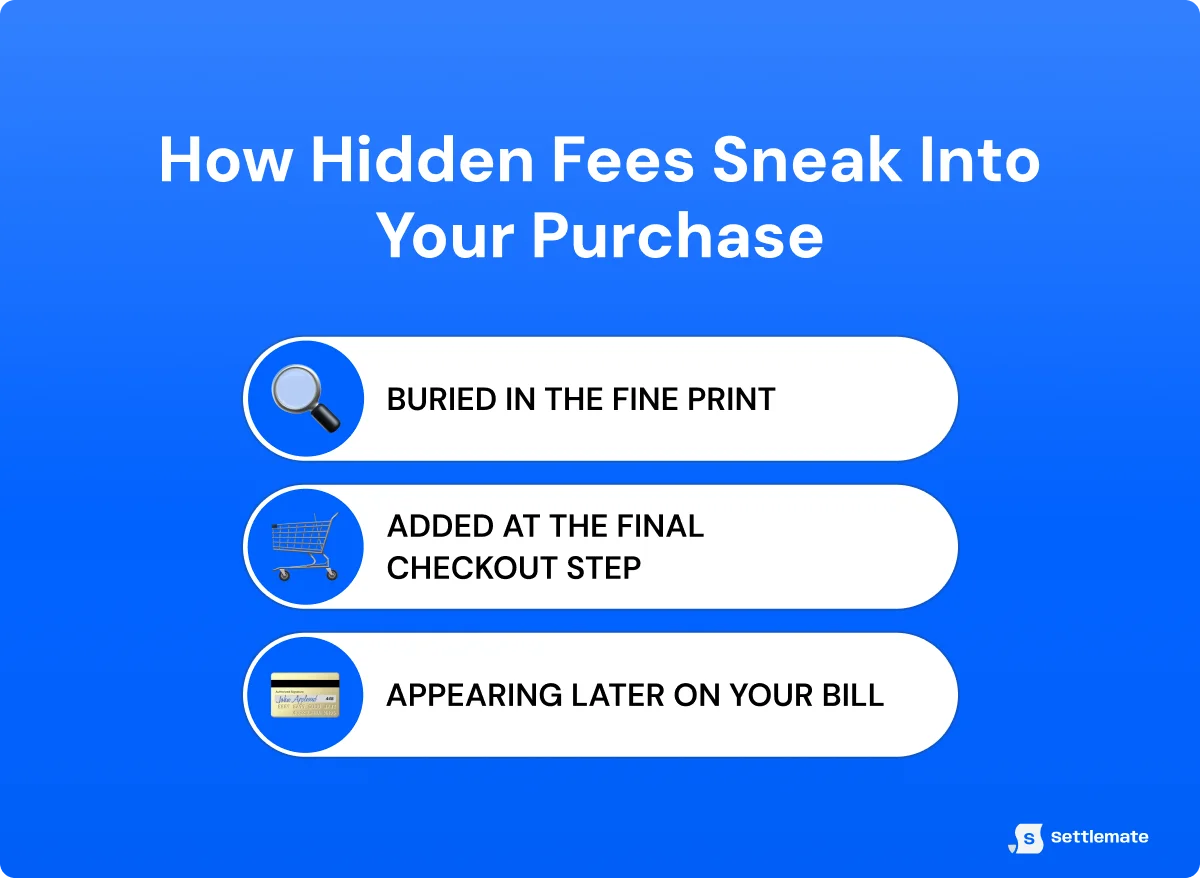

What are hidden fees?

Hidden fees are charges you don’t see when you agree to buy something, but you end up paying them anyway. They can be buried in fine print, slipped in at the final checkout step, or shown later on your bill with no warning at all.

Most of them are small enough to look harmless on their own—often under $10—but the real problem is volume.

One company adds a fee here, another includes a “service” charge there, and suddenly, you’re out hundreds of dollars a year without ever agreeing to it.

To help you understand how this works, the table below offers a quick overview of the most common hidden fees and where they tend to hide:

Hidden fees distort the real price until you’re already deep into the purchase. By the time you see the true total, you’ve mentally committed, and companies bank on you accepting it.

What is a hidden fees lawsuit?

A hidden fees lawsuit is a legal action that forces companies to return money they charged without proper disclosure.

While not every fee is illegal, failing to clearly and conspicuously disclose the full cost before payment is. Such deceptive pricing leads to lawsuits.

Consumers often assume these fees are “too small to fight.” However, all it takes is one customer to notice a pattern, a lawyer to dig in, and suddenly, you have an entire customer base standing behind the same claim.

That’s when those $5–$20 surprise charges turn into millions in recovery in total.

Plus, hidden fees lawsuits often force companies to fix the pricing tactics that got them sued in the first place.

Hidden fees lawsuit: Past examples

Some of the biggest brands in the country have been caught padding prices, burying fees, and misleading customers.

Here are some of the standout hidden fees lawsuit cases that showed exactly where these charges come from—and why consumers are fighting back:

Hidden fees lawsuits: 3 ongoing cases you can join right now

Regulators are trying to shut down hidden fees. For instance, the FTC rolled out a new rule in 2025 that forces ticketing platforms and short-term lodging sites to show the real price up front, thus putting an end to the so-called “bait-and-switch” pricing.

But even with tougher rules, hidden fees cases are still landing in court. Here are three ongoing ones you can join right now if you were hit with the same pricing tactics.

1. New York Community Bank’s double ATM and NSF fees

Flagstar Financial, formerly New York Community Bank (NYCB), was accused of quietly stacking fees on everyday customers between 2017 and 2024.

The hidden fees lawsuit says the bank charged multiple out-of-network ATM fees when customers checked their balance before withdrawing cash, and retry non-sufficient funds (NSF) fees each time the same payment was reprocessed. These weren’t disclosed the way they should’ve been, and customers ended up paying far more than the bank’s agreements allowed.

In response, customers filed a class action claiming that the fee structure violated the bank’s own policies. The bank didn’t admit wrongdoing, but ultimately agreed to a $1.23 million settlement.

The court has scheduled the final approval hearing for January 13, 2026, and the settlement administrator is already preparing distributions.

But can you join this class action lawsuit?

Well, you’re included automatically—no claim form required—if you had an NYCB checking account and were:

- Charged retry NSF or overdraft fees on check payments between March 2, 2017, and January 1, 2020

- Charged multiple out-of-network ATM fees after a balance inquiry between August 20, 2020, and February 20, 2024

If, however, you don’t want to be part of the settlement and prefer to keep your right to sue the bank on your own, you must opt out by December 15, 2025.

2. Airport parking’s undisclosed service fees

CAVU eCommerce, the company behind two popular airport parking websites, was accused of slipping in mandatory service charges that weren’t disclosed up front. California’s Honest Pricing Law requires businesses to show the real price before checkout, and the lawsuit claims CAVU broke that rule by revealing the fee only at the very end of the booking process.

After consumers challenged the practice, CAVU agreed to a $425,000 settlement.

As part of the deal, the company must now clearly and conspicuously disclose its service charges to comply with California law.

The court has scheduled the final approval hearing for December 1, 2025, and the claims window is currently open.

You can join this lawsuit if you meet the following conditions:

- You’re a California resident who booked airport parking through the relevant sites.

- You paid a mandatory service charge between July 1, 2024, and March 10, 2025.

To receive money, you must submit a claim by January 15, 2026. Keep in mind that the opt-out deadline has already passed.

3. Discover’s credit card misclassification fees

For years, Discover allegedly tagged certain consumer credit card transactions as commercial—a tiny classification change that made a very big difference for merchants.

Instead of paying the normal consumer-card interchange rates, businesses were charged the higher commercial rates every time one of these misclassified cards was swiped. The hidden fees lawsuit argues this wasn’t disclosed and caused merchants across the country to overpay for routine transactions.

Merchants pushed back, filing a class action claiming that Discover inflated costs through improper coding.

Discover denied wrongdoing but agreed to a $1.225 billion settlement, one of the largest interchange-fee settlements on record. The court has already laid out the approval schedule, with a final hearing set for May 20, 2026.

You can be included if you were an end merchant, merchant acquirer, or payment intermediary that processed or accepted a misclassified Discover transaction between January 1, 2007, and December 31, 2023.

To receive money, you must file a claim by May 18, 2026. If you want to keep your right to sue Discover individually, the opt-out deadline is March 25, 2026.

Hidden fees lawsuit: How to find out which cases you qualify for

New hidden fees investigations launch constantly. Lawyers are already looking into whether companies like Uber Eats, SeatGeek, and StubHub are violating state pricing laws through drip pricing, junk fees, or undisclosed add-ons.

In other words, the three open cases above are not the whole picture; they’re just what’s active today.

So, check in regularly, and see whether your purchases, bills, or subscriptions match a new hidden fees lawsuit. Here are three ways to do that.

1. Check manually

Hidden fees aren’t invisible fees. If you scan the right places, the red flags show up quickly.

Here’s where to look:

- Telecom bills – Phone or internet plans padded with “administrative,” “regulatory,” or similar add-on charges that never appeared in the advertised price

- Travel and ticketing offers – Resort fees, amenity fees, or “processing” charges revealed only at checkout

- Bank statements – Re-presentment overdraft fees, surprise NSF charges, or hidden spreads built into crypto trades

If the number you paid doesn’t match the number you were shown up front, search “[company name] hidden fees class action 2025” and see whether it’s already an active case.

2. Search online databases

You don’t necessarily have to start with your bills; you can head straight to the internet.

Scan major public databases that track open consumer cases and look for a match. Look up the companies you actually use: your phone provider, travel sites, streaming services, banks, delivery apps, and anyone else that touches your wallet.

Cases involving hidden fees appear across dozens of industries, and these databases regularly update active lawsuits, settlements, and new investigations.

3. Let an app do the work for you

If you don’t feel like combing through bills, searching case lists, or checking databases every few weeks, you can let an app do the heavy lifting for you.

Settlemate finds the claims you qualify for automatically and handles the annoying parts of the process so you don’t have to.

Here’s what the app offers:

- Instant eligibility matching: Answer a few quick questions, and Settlemate will scan its full database of open class-action settlements to show you exactly which ones include you.

- Lawyer-free filing: You can complete, sign, and submit your claim directly in the app with no legal forms or lawyer involvement.

- Real-time tracking: Settlemate allows you to see live updates on claim status, deadlines, and estimated payouts.

- Smart notifications: Get alerts when a new settlement fits your purchases or when an existing claim moves forward.

- Automatic receipt and email scanning: Settlemate detects eligible purchases for you, even from past orders you forgot about.

Settlemate handles the work most people never get around to, so you don’t miss money you’re legally owed.

Why you should use Settlemate to get your money back

Companies count on you missing the fine print. They count on you ignoring a $5 charge here, a “processing” fee there, and never connecting the dots. Those small hits add up, and when a hidden fees lawsuit forces companies to pay it back, you deserve every dollar that’s legally yours.

Settlemate makes sure you actually get it.

The app finds the claims you qualify for, auto-fills your forms, tracks your payouts, and handles the paperwork you’d normally avoid. If there’s cash on the table, Settlemate puts it in front of you.

And don’t worry: Settlemate’s pricing has no hidden fees, no surprise add-ons, and no fine-print tricks. Just a straightforward way to claim real money from class action settlements without hiring a lawyer.

Download the Settlemate app on iOS or Android and start claiming what’s already yours.