According to Experian, the average American carries $104,755 in consumer debt. That number is enough to overwhelm even solid incomes, turning everyday expenses into stress points and every paycheck into damage control.

That’s why so many people start looking for ways to reduce what they owe, not just manage it.

One option that often comes up is debt settlement.

You’ve probably heard of it as a way to pay less than you owe and finally free yourself from debt. Sometimes that’s true. Other times, it makes the situation worse.

So, what is debt settlement, how does it actually work, and when does it make sense?

This guide walks you through the process, the real pros and cons, and the alternatives, so you can make an informed decision.

Key takeaways

- Debt settlement is a last-resort tool, not a first move

It involves negotiating to pay less than you owe, but it usually only makes sense if you are already behind on payments, facing serious hardship, and out of better options like credit counseling or a debt management plan. - It can reduce balances, but the trade-offs are real

Successful settlements may cut balances by 30% to 60%. However, they often come with major downsides, including credit score drops, high fees, and potential tax bills on forgiven debt. - Outcomes are uncertain and can take years

Creditors aren’t required to agree, balances can grow while negotiations drag on, and the process commonly lasts three to four years with ongoing stress and financial uncertainty. - Many people are better served by safer alternatives first

Options like nonprofit credit counseling, debt management plans, consolidation, or even bankruptcy can offer clearer rules, faster relief, and less long-term damage, depending on your situation. - Increasing cash flow without added risk can change your options

Before settling debt, finding extra money can make other paths viable. Settlemate helps you claim money you are already owed from class action settlements, recalls, and refunds with no credit impact and minimal effort.

What is debt settlement?

Debt settlement is a process where you negotiate with creditors to accept less than the full amount you owe and consider the debt resolved.

While you can negotiate a settlement yourself, when people say “debt settlement,” they’re usually talking about hiring a company—sometimes called debt relief—to negotiate on their behalf.

This is typically a last-resort strategy that makes sense if you:

- Are at least three months behind on your payments

- Are dealing with serious financial hardship

- Can no longer keep up with minimum payments

- Have exhausted other repayment options

- Can set aside cash for a lump-sum offer

If you’re current on payments and managing your bills, settlement is rarely the right move.

Debt settlement also only applies to certain types of debt. Generally, you can only negotiate unsecured debt—balances that aren’t tied to any property that a lender can take back.

The table below should help you quickly determine whether your debt is eligible for settlement:

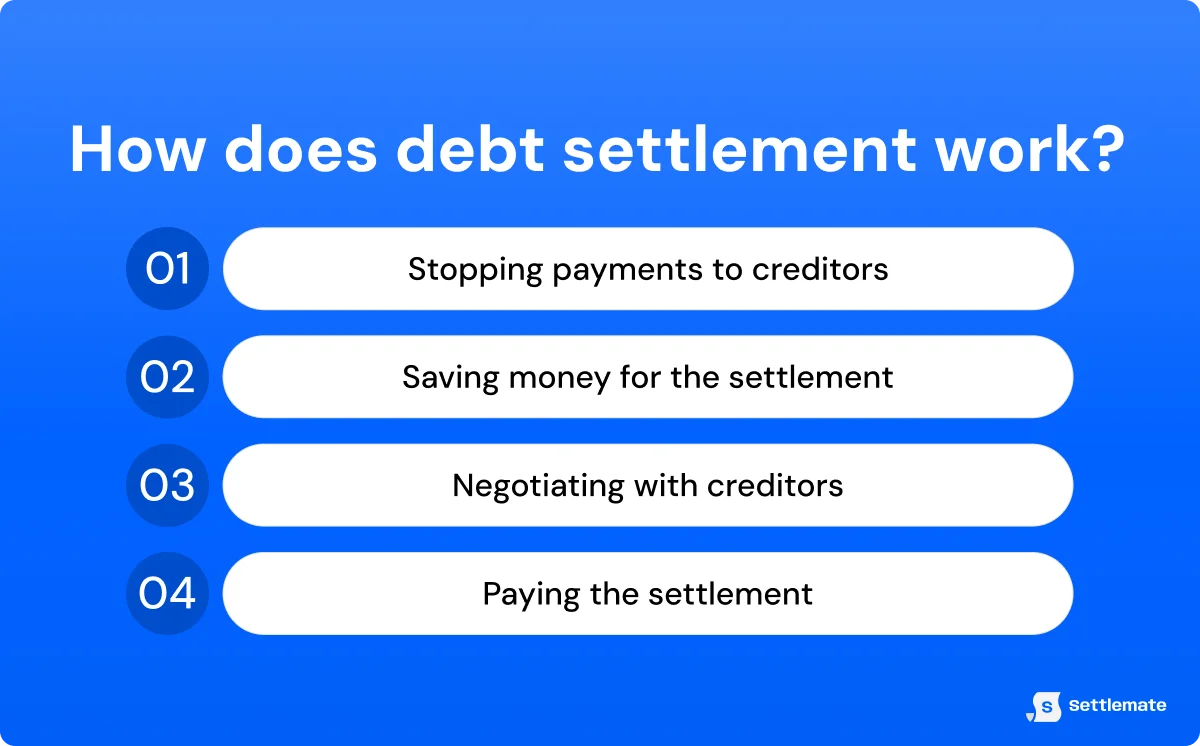

How does debt settlement work? 4 key steps

Debt settlement follows a fairly predictable path, which can be broken down into four key steps.

Step 1: You stop paying your creditors

To create leverage, payments to creditors are usually stopped. This allows accounts to become delinquent, which increases the chance a lender will agree to settle rather than risk getting nothing.

Step 2: You set aside money for settlements

Instead of paying creditors, you deposit money each month into a dedicated savings or escrow account. If you’re working with a settlement company, they may manage this account and collect their fees from it.

By law, companies must disclose upfront how much you’ll need to save before starting to negotiate.

Step 3: Negotiations begin

Once enough money is available, settlement offers are made to creditors.

The goal is to convince them to accept a reduced lump-sum payment, sometimes significantly less than the original balance.

Regardless of the amount offered, creditors aren’t required to agree.

Step 4: You pay the settlement

Once a creditor agrees to a settlement, you pay the negotiated lump sum, and the account is marked as settled. This means you’re no longer on the hook for the remaining balance, but the forgiven amount may count as taxable income.

When settling works in your favor: 6 pros of debt settlement

For people who are already overwhelmed and out of options, debt settlement can be a practical way to regain control. These are six key ways debt settlement can work in your favor when it’s used intentionally and at the right time.

1. Reducing the total amount you owe

When settlement works, creditors may agree to accept 30% to 60% of the original balance, wiping out the rest. That can mean saving thousands of dollars and finally seeing an endpoint, especially if interest has been doing more damage than progress.

2. Paying off debt faster than long-term repayment plans

Long repayment timelines are usually associated with secured debt like mortgages, but even unsecured debt can take decades to pay off when you’re stuck making minimum payments.

With debt settlement, the focus shifts to resolution, often allowing debts to be settled and closed within two to four years instead.

3. Avoiding bankruptcy

For many people considering debt settlement, the real choice isn’t between settlement and slowly paying everything back. It’s between debt settlement and bankruptcy.

When settlement works, it can provide a middle ground.

You resolve debts for less than you owe without filing a formal bankruptcy case, which can carry longer-lasting legal and financial consequences. Bankruptcy filings stay on your credit report for seven years under Chapter 13 or 10 years under Chapter 7, and the record can follow you even longer when applying for credit, housing, or certain jobs.

Debt settlement also gives creditors a reason to negotiate.

From their perspective, accepting a reduced payment can be better than risking partial repayment under Chapter 13 or nothing at all under Chapter 7.

4. Getting professional help negotiating with creditors

Negotiating with creditors takes persistence, timing, and pressure. A debt settlement service handles the outreach, back-and-forth, and paperwork, removing the burden from you and increasing the chances of getting a settlement actually accepted.

5. Putting an end to collection calls once debts are settled

Compared to financial outcomes like lower balances or faster payoff, this advantage might sound minor. But anyone who’s dealt with repeated collection calls knows how disruptive and exhausting they can be.

Once settlement is complete for a specific debt, creditors and collection agencies no longer have a reason—or a right—to keep calling about it. For many people, the relief alone makes debt settlement worth it.

6. Lowering the risk of lawsuits on delinquent debt

When unsecured debt goes unpaid long enough, lawsuits become a real possibility.

Debt settlement can reduce that risk by resolving accounts before creditors decide legal action is worth the cost.

While lawsuits aren’t guaranteed—and settlements aren’t either—creditors often prefer accepting a negotiated payment over spending time and money in court.

When settling backfires: 6 cons of debt settlement

Debt settlement can work in specific situations, but it should almost never be the first option you reach for. Its trade-offs are real, and in many cases, they can leave you worse off if you don’t fully understand what you’re signing up for.

These are the six key downsides to consider before making any decisions:

1. Damaging your credit score for years

Debt settlement almost always starts by missing payments on purpose, which doesn’t bode well for your credit score since payment history is the single biggest factor in how it’s calculated.

A missed payment can hurt your score within 30 days, with steeper drops coming at 60 and 90 days past due. By the time a settlement is reached, many people see their score fall 100 points or more, depending on where they started.

But the damage doesn’t end when the debt is settled.

Missed payments, charge-offs, collections, and settled accounts can all remain on your credit report for up to seven years from the original delinquency. That can make it harder—or more expensive—to qualify for credit cards, auto loans, or a mortgage long after the debt itself is gone.

If your credit is already severely damaged, the impact may feel less dramatic. But if you’re starting from a decent score, settlement can be a major setback.

2. Facing no guarantee that creditors will agree

Debt settlement is always voluntary on the creditor’s side. Creditors aren’t required to negotiate, and some outright refuse to do so. Even after months of missed payments, an offer can be rejected or met with collections or legal action instead.

3. Risking higher balances while negotiations drag on

While negotiations are ongoing, interest and late fees usually continue to pile up.

If a creditor delays or refuses to settle, your balance can grow, sometimes leaving you owing more than what you did when you started. Even when a settlement is reached, the damage from months of nonpayment has already been done.

4. Paying high fees that reduce or erase savings

Debt settlement companies typically charge 15% to 25% of the debt you enroll, not the amount they save you.

On a $20,000 balance, that can mean $3,000 to $5,000 in fees alone.

Since these costs don’t reduce your debt but go straight to the company, they can wipe out much of the savings from settling.

5. Owing taxes on forgiven debt

With most settlements, the question of tax treatment is unavoidable.

When a creditor forgives $600 or more through a debt settlement, the Internal Revenue Service (IRS) may treat that forgiven amount as taxable income.

For example, settling a $12,000 balance for $7,000 leaves $5,000 forgiven. The creditor is legally required to report that amount to the IRS, which may increase your taxable income for the year, even though you never received cash.

6. Dealing with long timelines, stress, and uncertainty

While debt settlement is often one of the fastest ways to resolve serious unsecured debt, it still isn’t quick by most standards.

The process can take up to four years, with no guarantees. During that time, balances may grow, credit remains damaged, and outcomes stay uncertain, which can take a real toll on your stress levels.

Other ways to deal with debt: 6 alternatives to debt settlement

If learning what debt settlement is makes you hesitant to move forward, the table below gives a concise overview of its main alternatives that might be a better fit for you:

A smarter alternative: Find money you’re already owed

One of the safest ways to improve your situation is to bring in extra money without taking on more risk. That doesn’t always mean a side hustle or working longer hours. Sometimes, it means claiming money that’s already yours.

That’s where Settlemate comes in.

Settlemate helps you find and claim money you’re legally owed from class action settlements, product recalls, airline issues, and similar refund opportunities, which most people miss entirely. The app will:

- Scan your email and receipts to find settlements you qualify for

- Match you instantly with open claims

- Auto-fill and submit claim forms for you

- Alert you when new opportunities open

- Track claim status, deadlines, and payouts in one place

There’s no negotiating, no credit impact, and no long-term commitment. Just overlooked money claimed with minimal effort.

If you’re looking for a lower-risk way to free up cash, download Settlemate for iOS or Android and see what your inbox has been hiding.