Banks are notorious for piling on hidden fees on Americans, and these aren’t pocket change.

In 2023, banks raked in $5.83 billion from overdraft and non-sufficient funds (NSF) fees alone, and that’s after regulatory pressure and policy changes. Back in 2019, before the crackdown, these same fees pulled in a staggering $11.96 billion.

The volume has since dropped, but the problem still exists. These unfair fees persist because they’re profitable, easy to hide, and often hit people who can least afford them.

But here’s the part banks don’t advertise: many of these charges are refundable.

Sometimes, all you have to do is ask. Other times, regulators will step in—like when they forced financial institutions to return over $120 million to customers in 2023.

If you want to be part of the 2026 refund numbers, this guide shows you which hidden bank fees you can challenge and how to actually get that money back.

Key takeaways

- Many “hidden” fees are refundable if they were unexpected or poorly disclosed

Overdraft fees, NSF fees, statement fees, maintenance fees, ATM charges, and several smaller service fees can all be reversed if they weren’t clearly explained or if bank systems caused the issue. - You have real leverage when disputing unfair fees

If the fee breaks the bank’s own rules, contradicts TISA disclosure requirements, or results from timing issues or posting errors, banks routinely issue refunds. Long-time customers and near-miss situations have especially strong cases. - A structured approach dramatically increases your refund success rate

Identify the fee, check the bank’s terms, gather proof, and contact customer support through the fastest channel. If denied, escalate to supervisors, executive support, or regulators like the CFPB, which banks take seriously. - You don’t have to fight these battles alone

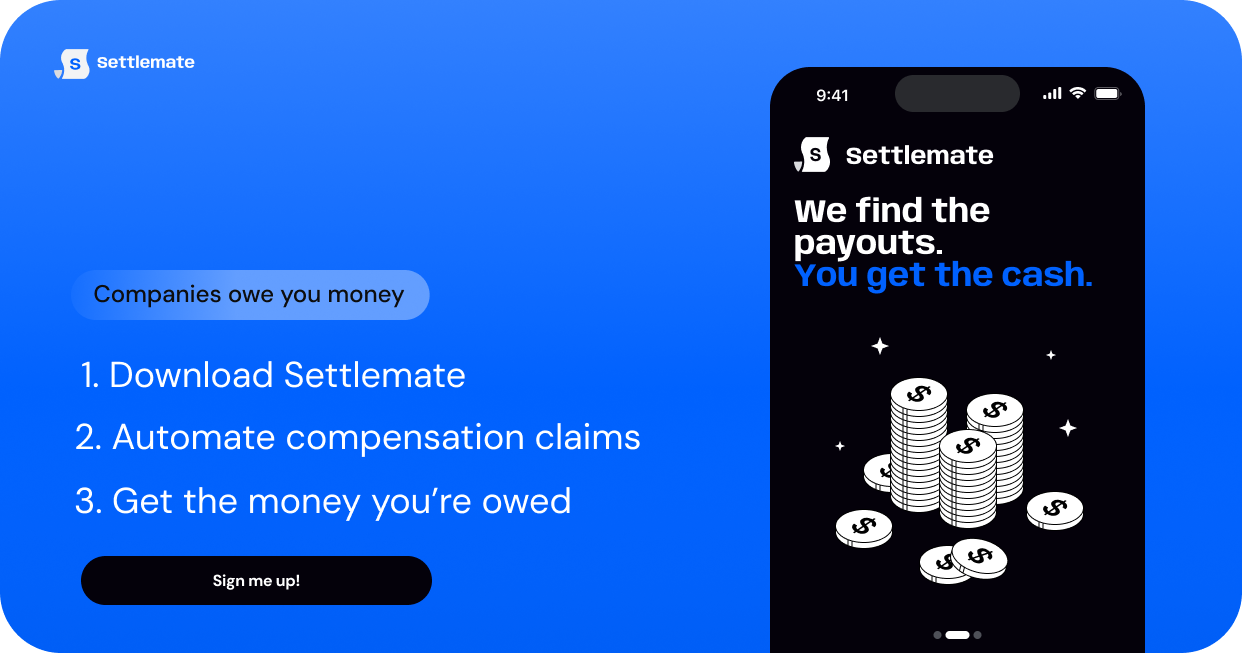

Tools like Settlemate automate the hard part by scanning your history for refund opportunities, handling the paperwork for eligible class actions, and tracking your payouts.

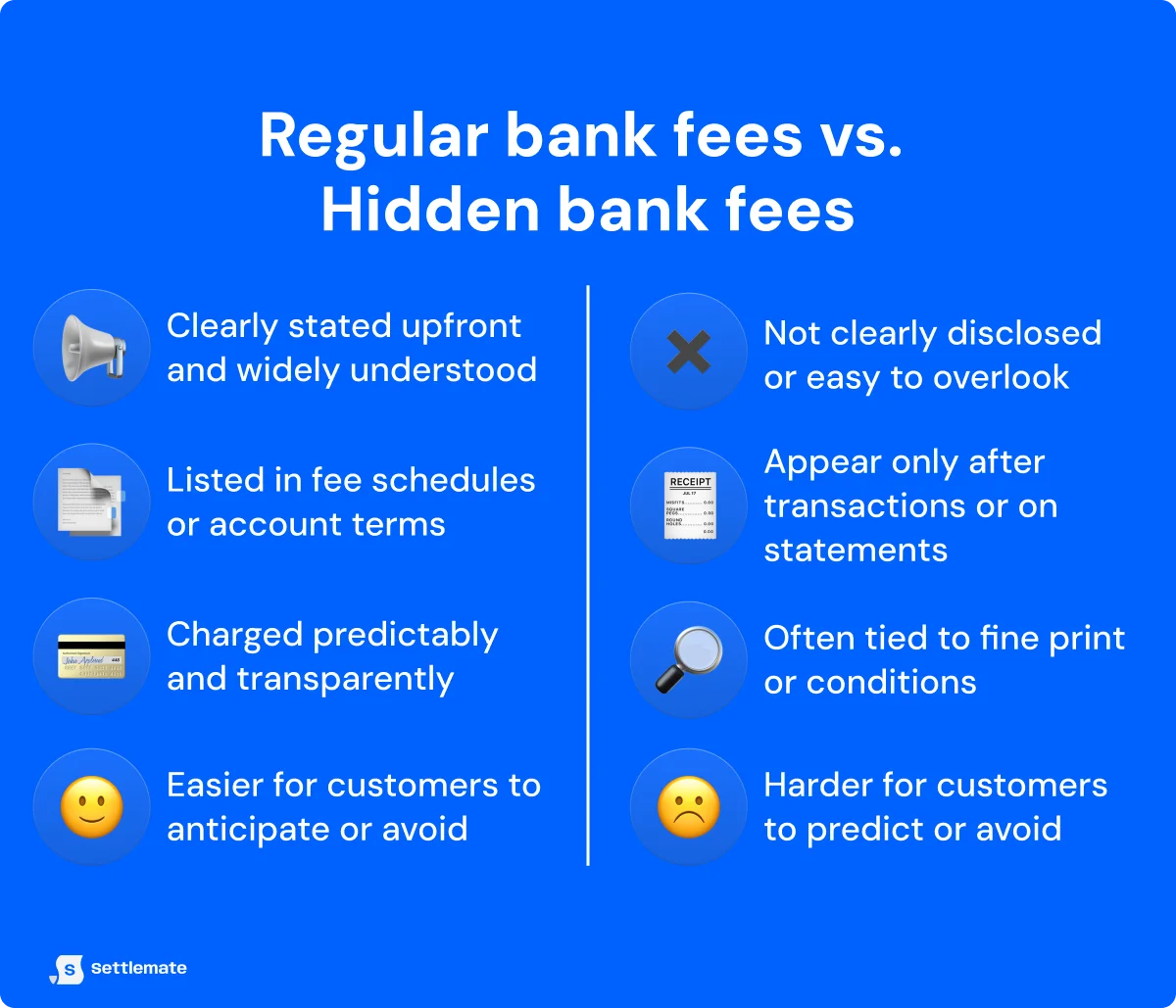

What are hidden bank fees?

Hidden bank fees are unexpected charges that show up on your account even though you didn’t clearly consent to them, or didn’t understand the conditions that triggered them.

These fees are problematic because the Truth in Savings Act (TISA) requires banks to clearly disclose every fee, yet many customers only learn about these charges after they’ve been hit with one.

That gap between what’s “technically disclosed” and what people actually understand is exactly what regulators are targeting.

Which hidden bank fees can you claim a refund for?

You can claim refunds for a wider range of hidden bank fees than most people realize. Below are the specific fee types you can dispute and what makes each one eligible for a refund.

1. Overdraft fees

Overdraft fees are the most commonly disputed hidden bank fees, and your best shot at a refund. These are charges your bank adds when it lets a transaction go through even though you don’t have enough money to cover it.

Here’s an example.

Your account balance sits at $82. Overnight, two transactions hit: a $60 subscription renewal and a $40 debit purchase from earlier in the day. The bank approves both, covering the missing $18—a privilege for which you are charged an overdraft fee.

The exact overdraft fee depends on your bank and account type, but they typically range between $10 and $35 per overdraft.

The core issue with these fees is that overdrafts are often unavoidable in practice.

Timing delays, settlement orders, and temporary authorizations can cause a transaction to look approved at the time you swipe, and then overdraft after it settles. This is the CFPB-flagged APSN (Authorize-Positive, Settle-Negative) scenario, where consumers have no reasonable way to anticipate the fee.

Besides these timing quirks, you have a strong case for a refund if:

- The fee wasn’t clearly disclosed under TISA requirements.

- The bank recently changed its overdraft policy and didn’t notify you clearly.

- Multiple small transactions triggered a cascade of fees.

- You brought your account positive quickly (the same or next day).

- You’re a long-time customer with no history of repeated overdrafts.

2. Non-sufficient funds (NSF) fees

Unlike an overdraft fee, where the bank approves the transaction and charges you for covering the shortfall, an NSF fee happens when the bank declines the payment entirely because you don’t have enough money to cover it.

But if the bank didn’t cover the amount for you, why are you still getting charged?

Because the bank still has to process, return, and report the failed transaction.

Historically, banks charged an NSF fee to cover the “administrative cost” of sending that payment back unpaid. In reality, regulators have found that the actual cost to the bank is minimal, which is why NSF fees were labeled junk fees and largely eliminated.

If, however, your bank didn’t get the memo, you have a strong case to claim a refund under the following conditions:

- You were charged multiple NSF fees for the same transaction.

- You didn’t receive notice that the transaction would be re-attempted.

- The fee wasn’t clearly disclosed or was in conflict with TISA requirements.

- The failed payment resulted from bank timing issues, posting delays, or merchant errors.

- You were charged under the old policy when your bank had NSF fees.

3. Statement fees

Statement fees are charges your bank adds when it prints and mails a paper account statement instead of delivering it electronically.

They typically run between $2 and $5 per month, and many customers don’t realize they’re being billed for them. Although these fees are typically small, regulators flagged them because some banks charged them even when they didn’t actually print or mail the statements.

If this happened to you, too, you’re eligible for a refund. The same goes if:

- You were billed returned mail fees for statements that the bank never attempted to send

- You didn’t knowingly opt out of electronic delivery

- Your bank has shifted to paperless policies but failed to notify you of the paper-statement charges

4. Maintenance fees

Monthly maintenance fees are the charges banks add just to keep your account active. They’re not truly hidden since banks are legally required to disclose them, but they’re often unfair in practice.

These fees are usually supposed to be avoidable if you meet certain conditions, such as maintaining a minimum balance, hitting a direct deposit requirement, or using the account a set number of times.

The problem is that customers often aren’t clearly notified when they miss a requirement by a hair. For example, your direct deposit might hit just one day late, but the fee is still automatically deducted.

Some banks also bury the waiver rules deep in disclosures, leaving customers confused about why the fee appeared at all.

As a result, you might be eligible for a maintenance fee refund under these conditions:

- You nearly met the waiver requirement.

- You met the requirement, but the bank’s system misread your activity (happens frequently with minimum-balance thresholds).

- The bank didn’t clearly disclose the fee or the waiver criteria.

- You were switched into a new account type without understanding that the fee structure had changed.

- You’re a long-term customer with a clean account history.

5. ATM fees

You’ll usually get charged ATM fees when you use a machine outside your bank’s network. Most major banks charge $2.50 to $3.00 per withdrawal, and the ATM owner often adds its own fee on top.

You should be able to get a refund for out-of-network (OON) ATM fees if:

- The ATM malfunctioned or didn’t dispense the full amount.

- The fee was not properly disclosed on-screen before the transaction.

- You were charged for an ATM interaction you didn’t make (e.g., card skimming, unauthorized withdrawal).

- Your bank typically reimburses ATM fees but missed one.

- You’re a long-time customer and ask for a courtesy refund.

6. Other fees

There are additional bank fees that may be refundable when they’re applied under unfair, unclear, or improperly disclosed circumstances.

Refunds are less common in these cases, but if any of these fees contradict the bank’s own policies or blindsides you, you still have leverage:

- Early account-closure fees: Banks can charge these when you close a new account too quickly (usually within three to six months).

- Stop-payment fees: Banks often charge around $30 to stop a check or Automated Clearing House (ACH) pull.

- Returned deposit item (depositor) fees: These hit when you try to deposit a check that bounces.

- Minimum balance fees: Banks assess these when your balance dips below a required threshold.

How to claim a refund for hidden bank fees

Claiming a refund for hidden bank fees doesn’t cost you anything, your bank won’t penalize you for raising the issue, and if the charge was unfair, you have a legitimate shot at getting it reversed.

Here’s how to go about it, step by step.

Step 1: Identify the fees on your statements

Scan your monthly statements line by line. Banks often mask fees under abbreviations like:

- OD (overdraft)

- NSF (non-sufficient funds)

- MNT (maintenance)

- ATM OON (out-of-network ATM)

If a charge looks unfamiliar or unclear, flag it immediately.

Step 2: Check your bank’s rules

Pull up your account’s fee terms: the disclosure you received at signup or the version posted on your bank’s site. Look for the conditions that trigger the fee and the situations where the bank says it can waive it.

If the charge doesn’t line up with their stated policy, or if you met (or nearly met) the waiver requirements, you already have a strong argument.

Step 3: Gather proof

Have the exact details ready: the fee amount, the posting date, and the transaction it ties to. Save screenshots of statements, app activity, deposit confirmations, or anything that shows the bank misapplied its own rules. The clearer your evidence, the faster the refund conversation.

Step 4: Contact your bank

It’s time to actually ask for a refund, and you can do so by contacting your bank through the following channels:

Regardless of your chosen method, keep it direct: state the fee, the date, and the reason it shouldn’t have been charged. Then, ask for it to be reversed.

Step 5: Escalate if needed

If the frontline support won’t budge, you might need to escalate the matter. The higher you go, the more authority you’re dealing with, and the better your odds of getting the fee reversed.

This might include:

- Asking for a supervisor: Frontline reps often can’t override fees, but supervisors can.

- Reaching out to executive customer care: Larger banks have escalation teams tied to the CEO’s office; a concise email can route your case there.

- Posting to public channels: A calm, factual post tagging the bank’s help account can prompt faster follow-up.

Step 6: Involve the law

If the bank still won’t reverse the fee, it’s time to escalate outside their customer-service loop.

Your strongest options include:

- Filing a CFPB complaint: Go to the CFPB’s online portal and submit a clear summary of what happened. The regulator will send your case directly to the bank’s high-level review team.

- Escalating to your state banking regulator: Every state has an agency that oversees consumer banking issues, and they can pressure the institution to resolve unfair fees.

- Joining a class action: When a bank’s fee practices violate law or policy, hidden fees lawsuits form. If you qualify, you can recover money automatically.

Your hidden bank fees defense plan

Dealing with hidden bank fees is annoying, sometimes expensive, and almost always avoidable. That’s why you should do everything you can to avoid them in the first place, like:

- Turning on low-balance alerts

- Checking your balance before larger purchases

- Opting out of overdraft where it makes sense

- Favoring banks that don’t weaponize fees against you

You should also utilize an automatic tool like Settlemate to prevent you from missing anything.

Here’s what Settlemate does for you:

- Finds money you didn’t know about: Settlemate reviews your purchase history and matches it against active class actions, refund programs, and regulator-driven payouts.

- Handles the boring paperwork: The app fills in claim forms with the right details, asks you only for what’s missing, and sends them off in a few taps.

- Keeps every claim moving: You see each claim’s status from submitted to paid, with updates when anything changes.

- Makes sure you don’t miss deadlines: The app flags closing windows and new eligible cases so you’re not leaving money on the table.

Download Settlemate on the App Store or Google Play and start turning hidden fees and ignored notices into actual cash back in your account.